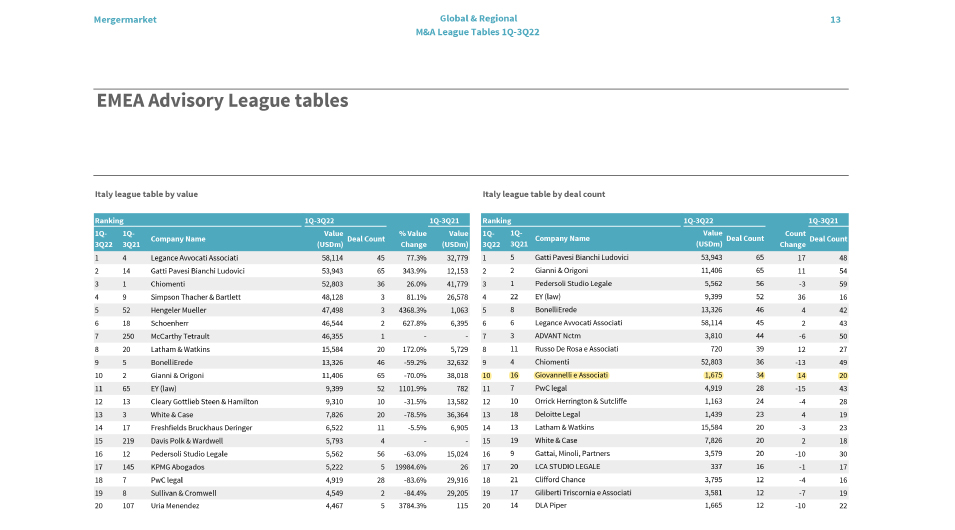

Giovannelli e Associati is ranked again in 1Q-3Q22 Global & Regional League Tables according to Mergermarket

13/10/2022

Giovannelli e Associati with IDeA Agro on the investment in Apicultura Vangelisti

11/11/2022

I. Foreword

On 20 October 2022, the Italian tax authorities released a long-awaited update to the general guidelines concerning the Italian tax regime of trusts (the “New Guidelines”), almost one year after a draft version was issued for public consultation to collect inputs from any interested party.

The New Guidelines are to be welcomed as a critical document which, on one side, updates the last general guidelines issued in 2007 and 2010 and, on the other, aims at consolidating and harmonizing a long list of official (and non-official) rulings issued on trusts over the years to address specific cases raised by taxpayers.

Remarkably, the tax authorities acknowledge some of the key principles upheld by the Italian Supreme Court on the most debated issues of the tax regime of trusts and focus particularly on international cases (since, in late 2019, the rules on taxation of distribution from foreign trusts were substantially revised by Law Decree no. 124/2019).

The New Guidelines recognize the different types of trusts used in wealth planning and endeavor to clarify the key features of their Italian tax regime, namely: (i) income taxation, (ii) indirect taxation, (iii) special purpose trusts (iv) tax reporting and (v) property taxation.

II. Income taxation

The New Guidelines confirm that the settlement of goods and rights into a trust generally does not qualify as a taxable event and that in principle the relevant tax cost (of the settlor) is transferred to the trust accordingly (to avoid cases of double non-taxation). Exceptionally, the settlement into a trust of (a) selected financial assets or (b) goods and rights held by an entrepreneur may trigger taxable income in the hands of the settlor (and VAT, where applicable).

Trusts qualify as “opaque” and “transparent” depending on the rights to distributions of trust’s income granted to the beneficiaries and are subject to a different tax regime accordingly. The New Guidelines analyze separately Italian and non-Italian tax resident trusts.

Being trusts taxable entities for corporate income tax purposes, Italian tax resident trusts are subject to corporate income tax on income determined on a worldwide basis, while non-Italian tax resident trusts are subject to corporate income tax on income sourced within the Italian territory (based on domestic rules).

With regard to Italian tax resident trusts, the New Guidelines confirm that:

- distributions from an opaque trust to beneficiaries do not trigger a taxable income (in the hands of the latter), unless the trust qualifies as a business entity: in the latter case, distributions of trust’s income are deemed as akin to dividends and subject to a withholding tax of 26% accordingly;

- transparent trusts’ income accrues directly to qualifying beneficiaries and is taxed in the latter’s hands at standard proportional and progressive rates up to 43% plus local surcharges (hence, trusts are looked-through and the relevant distributions are disregarded); however, beneficiaries may benefit from tax selected exemptions and tax incentives generally available in case of direct investments.

With regard to non-Italian tax resident opaque trusts (or entities qualifying as akin to trusts based on a case-by-case analysis), the New Guidelines confirm that distributions to Italian resident beneficiaries do not trigger a taxable income in the hands of the latter. However, if trusts are established in States or territories applying a nominal taxation of their income lower than 50% of the corresponding Italian taxation on the same income, the following regime applies to Italian tax resident beneficiaries:

- distributions of “income” (sourced worldwide) qualify as “income from capital” subject to individual income tax at standard proportional and progressive rates (up to 43% plus local surcharges);

- distributions of “capital” do not trigger a taxable income;

- absent clear evidence of the nature of the distribution, the same is deemed as “income” (determined pursuant to Italian rules) and is taxable in the hands of the receiving beneficiary. To this end, the trustee is required to keep adequate accounting and non-accounting records of income and capital (e.g. bank statements);

- the assessment of the foreign trusts’ nominal taxation: (a) is carried out when income is derived by the trust, (b) covers special tax incentives applicable to trusts, and (c) is subject to a detailed review of the place of management of the trust, its main purpose and its tax residency status (pursuant to the relevant domestic laws and applicable double tax treaties). Contrary to the wording of the law, the New Guidelines note that the same analysis may extend to trusts established in EU and EEA member States, e.g. if they benefit of full tax exemption regimes reserved to “offshore” trusts (such as in Cyprus).

For both low-taxed opaque and any transparent foreign trusts, the New Guidelines point out that income taxable in the hands of Italian resident beneficiaries is determined on a worldwide basis, but if the same has already been taxed in Italy in the trust’s hands, beneficiaries will not suffer income taxation on the same amount.

Finally, trusts treated as fiscally interposed entities according to the official guidelines issued in the past by the tax authorities are disregarded and income is deemed as directly derived by the settlor or the beneficiaries subject to a case-by-case analysis. The New Guidelines clarify that distributions from fiscally interposed trusts to Italian resident beneficiaries never qualify as taxable events unless they concern income that has not already been taxed in Italy.

III. Indirect taxation

The New Guidelines emphasize the tax aspects of all the key stages of the lifespan of a trust, notably: trust set-up, settlement of goods and rights into the trust, trust management, attributions to beneficiaries and replacement of trustee (or protector). The focus is on inheritance and gift tax, registration tax, mortgage and cadastral taxes.

Remarkably, the tax authorities have radically changed their long-established approach to indirect taxation of trust and conform to the latest principles upheld by the Italian Supreme Court which, in a nutshell, consider a taxable event only the effective capital increase (“effettivo incremento patrimoniale”) of the trusts’ beneficiaries.

Accordingly, while the settlement of goods and rights into a trust does not entail an immediate and actual transfer of the ownership of such asset, the final transfer of the same to the beneficiaries shall trigger the application of the inheritance and gift tax (as well as mortgage and cadastral taxes if Italian properties are involved). In this respect, the New Guidelines point out the following:

- trust set up: the trust deed is subject to Italian registration tax at the fixed amount of 200€ (in principle also in case the deed is formed abroad). However, if identified beneficiaries are granted from the outset a full and due right to claim distributions from the trust at any time, inheritance and gift tax may apply at the standard rates, subject to a (crucial) case-by-case analysis of the trust deed and any other relevant circumstances to distinguish between “right” and “mere expectation”;

- settlement of goods/rights into the trust: each deed of settlement of goods/rights into the trust is subject to the same treatment of the trust deed (i.e. registration tax equals to 200€). The authorities pinpoint that such settlement may be deemed as a disposal triggering a forfeiture of selected indirect tax incentives benefited by the settlor (such as the so called “prima casa” regime in case a qualifying residential property is settled into the trust);

- attributions to beneficiaries: attributions of goods and rights qualifying as “capital” to the beneficiaries are subject to inheritance and gift taxes at the current standard rates. Remarkably, inheritance and gift tax are determined based on the family relationship (between the settlor and each relevant beneficiary) and the settlor’s residency status existing at the time of settlement of the goods/rights concerned into the trust. Therefore, such attribution may benefit from the tax allowances (up to 1,000,000€ direct line relatives) or fall outside the territoriality scope of inheritance and gift tax if the settlor was non-Italian tax resident and the attribution concerns goods located abroad. Moreover, subject to a case-by-case analysis, beneficiaries may have access to selected tax incentives generally applicable in case of gifts or succession (e.g. the so called “prima casa” regime);

- former attributions to beneficiaries: whereby the parties involved conformed to the past approach of the tax authorities and taxed the settlement of goods and rights into the trust at the standard rates, the New Guidelines identify two scenarios: (i) final tax payments and (ii) provisional tax payments. In the first scenario, the subsequent attribution of the same goods/rights to the original beneficiary will not trigger an additional taxation (and no right to a tax refund arises, save for certain exceptions). Conversely, in the second scenario, subsequent attributions of goods/rights different from those already taxed or attributions to beneficiaries different from those originally identified have to be subject to inheritance and gift taxes at the standard rates;

- trust management: deeds executed by the trustee on behalf of the trust are generally subject to registration tax at applied at the standard rates. The authorities pinpoint that the trust has not access to selected tax incentives generally applicable in case of gifts or succession in the hands of beneficiaries or heirs respectively (e.g. the so called “prima casa” and “prezzo-valore” regimes);

- replacement of trustee (or protector) or appointment of a new one: the relevant deeds are generally subject to registration tax at the fixed amount of 200€.

In the tax authorities’ view, if Italian properties are involved, mortgage and cadastral taxes would apply at the standard rates in the same cases mentioned above regarding inheritance and gift tax.

Moreover, similar principles generally apply also to special purpose trusts, depending on the circumstances. Notably, the New Guidelines clarify that in case of (i) a trust set up to secure settlor’s debts, registration tax applies upon the trust formation at the proportional rate of 0.5% of the secured obligations and (ii) a trust set up to repay the settlor’s debts, no taxation arises from the final attribution of the trust’s outstanding assets to the settlor.

Finally, contrary to the conclusions reached by the tax authorities in a ruling recently published, trusts treated as fiscally interposed entities are disregarded also for indirect tax purposes in case of demise of the settlor.

IV. Tax reporting and property tax on foreign investments

The New Guidelines confirm that the obligation to report annually assets and investments held abroad generally arises in the hands of Italian resident trusts (regardless of their status as “opaque” or “transparent”) and the Italian resident ultimate beneficial owners of trusts, as identified by the relevant Italian anti money laundering legislation (as well as in the OECD Common Reporting Standard). In this respect, it is also clarified that:

- Italian trusts are in principle not subject to such reporting obligation if all the trust fund is attributable to Italian resident ultimate beneficial owners required to comply with the same reporting obligation;

- the ultimate beneficial owner of trusts are only those beneficiaries who are clearly identified or can be easily identified by the trust deed or any other relevant document (e.g. those included in classes of beneficiaries);

- the reporting obligation arises in the hands of beneficiaries having a right to request the trust a distribution of income or capital;

- in case of a fiscally interposed trust, such obligation arises only in the hands of the Italian resident substantial owners of the trust fund (“interponente”).

The tax authorities interpret the law to exclude from these reporting obligations (i) holders of subsequent interests into the trust (e.g. the heirs of living beneficiaries), unless a case-by-case analysis demonstrates the opposite; and (ii) settlor, trustee and protector.

The reportable information varies depending on the trust’s nature:

- in case of discretionary trusts, only the values made available by the trustee on the foreign assets and investment held by the trust;

- in case of non-discretionary trusts, the value of all foreign assets and investment held by the trust.

Finally, the New Guidelines confirm that Italian resident “opaque” trusts qualify as entities subject to the property taxes on foreign real estate (so called “IVIE”) and financial investments (so called “IVAFE”), rather than their Italian resident beneficiaries.

It is not clear whether (i) the same principle applies apply to Italian resident “transparent” trusts and (ii) Italian resident commercial trusts are exempted from such obligation (such as Italian commercial entities). Both cases should be confirmed based on a grounded interpretation of the law and the contents of the New Guidelines.

V. Going forward

The New Guidelines clarify several aspects of the general tax regime of Italian and non-Italian trusts and, at the same time, require all the parties involved a detailed review of their position and level of compliance with the Italian laws.

In this context, it is the tight time to start re-examining existing trust structures having connections with Italy for being fully compliant with Italian laws or becoming more efficient from an Italian wealth planning angle.

Should you need any further information or clarification, please contact giorgio.vaselli@galaw.it or eugenio.romita@galaw.it